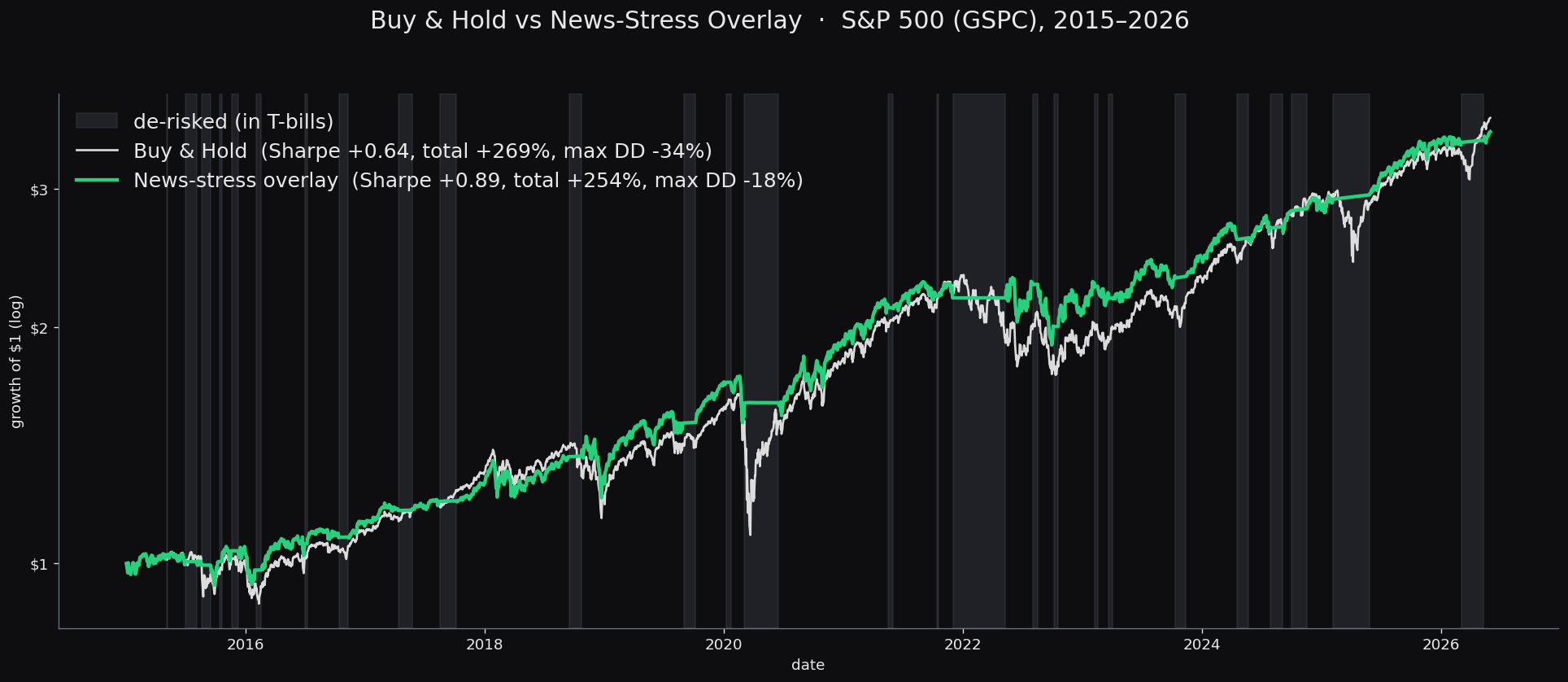

We built a risk-on/risk-off trading signal from the NOSIBLE event database that measures how much of the global news flow is about market-stress themes, holding equities when that reading is low and moving to T-bills when it spikes. Selected on 2010 to 2013 and tested on an untouched 2015 to 2026 window, it held the S&P 500's buy-and-hold return (+254% versus +269%) while cutting the maximum drawdown from −34% to −18% and raising the Sharpe ratio from 0.64 to 0.89. The same rule transfers unchanged to the Nasdaq and the Russell 2000.

2026-06-169 min read